CoreLogic Australia HVI Recorded its 4th consecutive decline in August. Is it now a buyer’s Market?

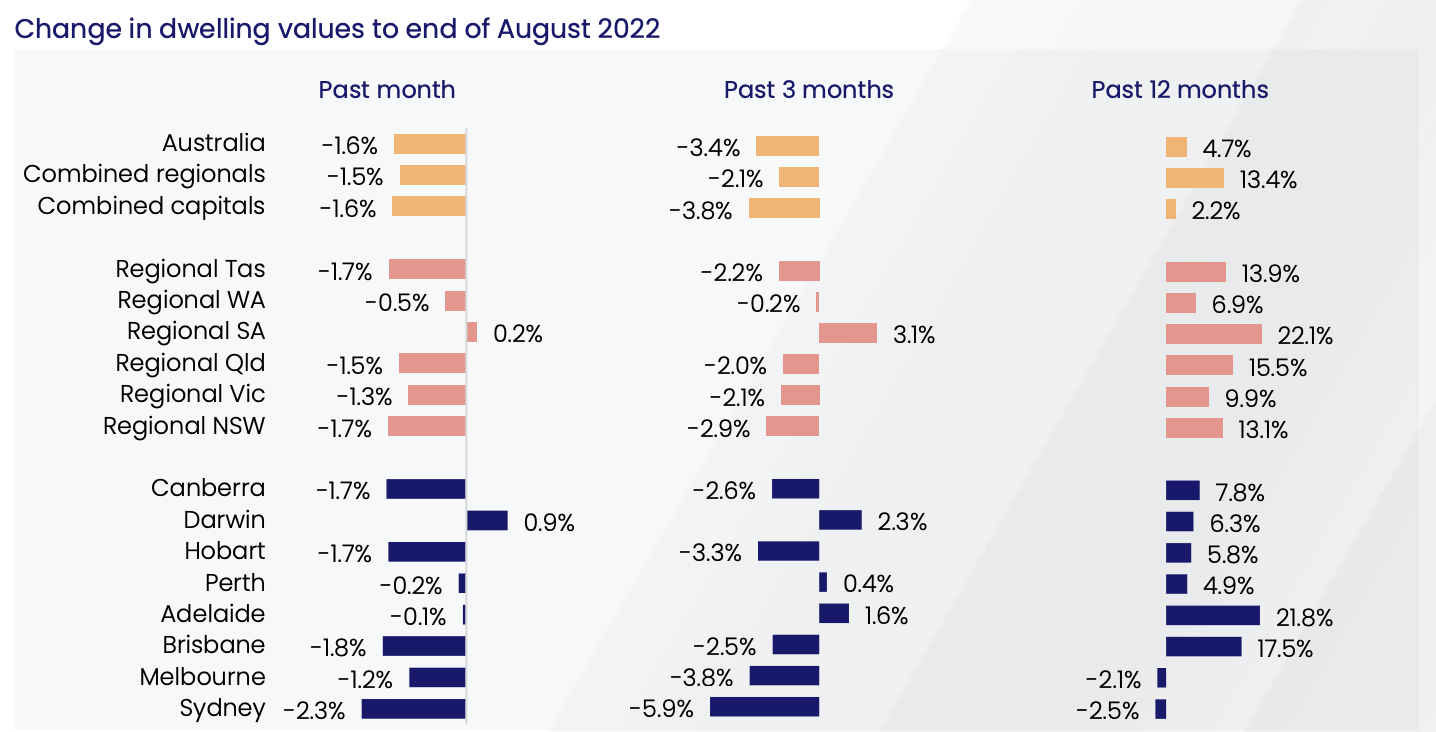

“CoreLogic’s national Home Value Index (HVI) recorded a fourth consecutive month of decline in August, with the downturn accelerating and becoming more geographically broad-based. Down - 1.6% over the month, the national index recorded the largest month-on-month decline since 1983.”

“As borrowing power is eroded by higher interest rates and rising household expenses due to inflation, it’s reasonable to expect a further decline in consumer confidence and lower housing demand,” Mr Lawless said.

The positive to lower housing prices is an improvement in some housing affordability measures, with the time needed to save a 20% deposit fall for the first time by about three months in Sydney 13.7 years and Melbourne 11.1 years in almost two years across the capital cities, while the dwelling value to income ratio also declined. As housing values trend lower and incomes rise, we expect to see a further reduction in these barriers to entering the housing market. Click on this link to see the full CoreLogic ANZ Housing Affordability Report.

The heat has well and truly come out of the market across all sectors except for Regional South Australia and Darwin. Both of these areas recorded slight growth of 0.2% and 0.9% receptively. All other capital cities and regions recorded negative growth for August.

Is it now time to buy? How much stock is on the market?

Since October last year, borrowers were required to demonstrate an ability to repay their debt under a mortgage rate scenario with an interest rate three percentage points higher than the current rate (2.5 percentage points before October 2021). Can you afford to stay out of the market? As with every interest rate rise, it limits the buyers borrowing power. The trend has reversed, and buyers are in control, but can they still afford the property they desire? We know banks are looking for new customers, and approvals are not taking as long as before. Are we at the bottom of the market? No, there will be a few more extra interest rate rises to come, but will you be able to afford the serviceability? Reserve Bank of Australia raised it’s cash rate to 2.35% on the 7th of September.

See our Mortgage Specialist, Adam Kingston’s Blog, on precisely this scenario.

Will your desired property be affected by these rises and see a price drop, or will you just have less money to borrow from the bank? Remember, Blue Chip Properties don’t go down; they retain their value because they are desirable. In some areas, there is more stock on the market; we’ve been told by our buyer’s agents from Milk Chocolate Property that you can pick and choose, especially for investment properties and further towards the end of 2022 new builds will enter the market.

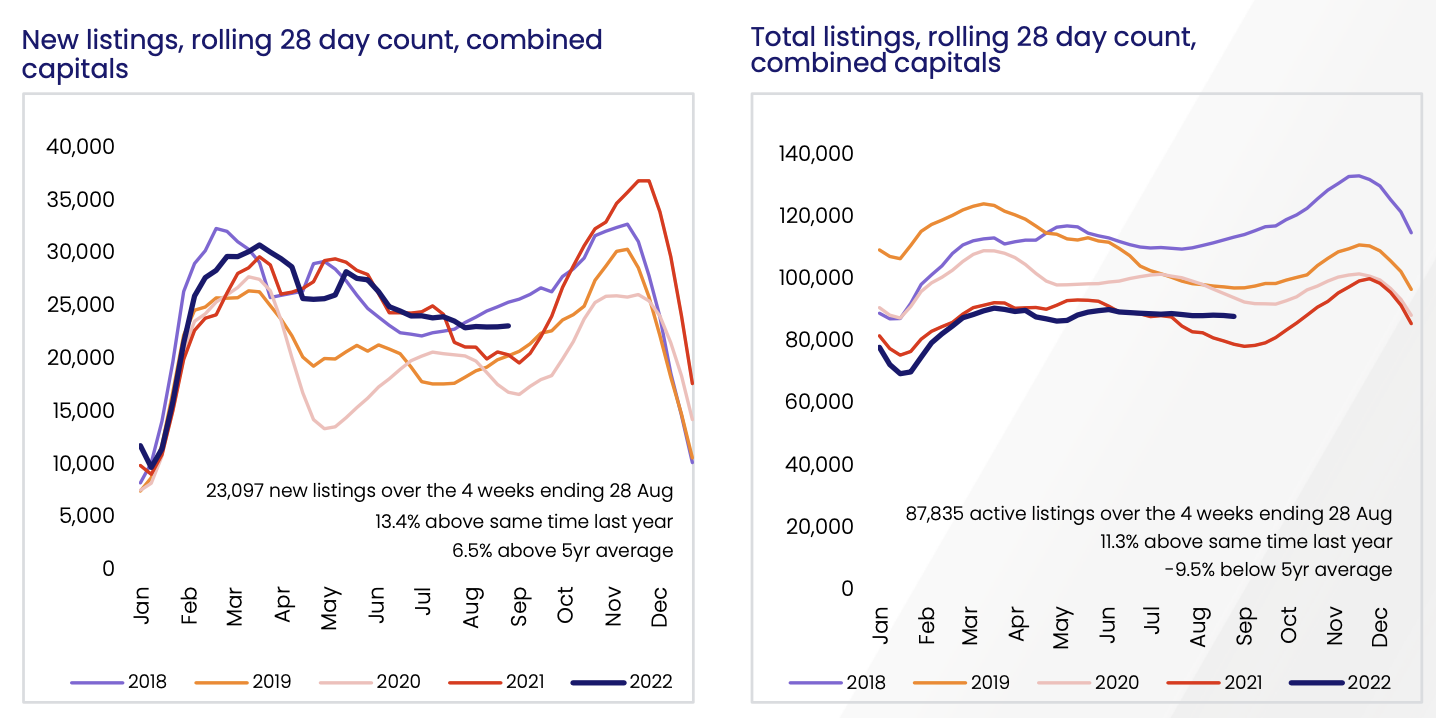

It is an excellent time to buy with stock returning to the market with 23,097 new listings over the four weeks ending on 28th August, which is 13.5% above the new listings recorded last year and 6.5% above the 5yr average. There were 87,835 active listings over the four weeks of August, 11.3% above the same time last year but -9.5% below the 5yr average. It is not all equal; in some areas, there is still limited stock. When the market is in decline, history indicates that Blue Chip Properties hold their value as vendors traditionally are under less financial pressure to sell. In a buyer’s market, you can negotiate better terms for your contract when purchasing your property. The Spring Selling Season is almost here, giving you more choices and improved buying power.

Investment Properties have seen a significant increase in rents in both houses and units. Brisbane with the highest change of 14.1% increase in Houses and Melbourne with 12.9% annual increase in rents for units.

“This trend is reversing as tenants become more willing to rent in higher density situations, especially in Sydney and Melbourne where unit rents are now rising at a much faster pace than house rents,” Mr Lawless said. “Potentially, we are seeing the first signs of smaller rental households that formed earlier in the pandemic reverting back to larger households or utilising higher density rental options to combat worsening rental affordability.”

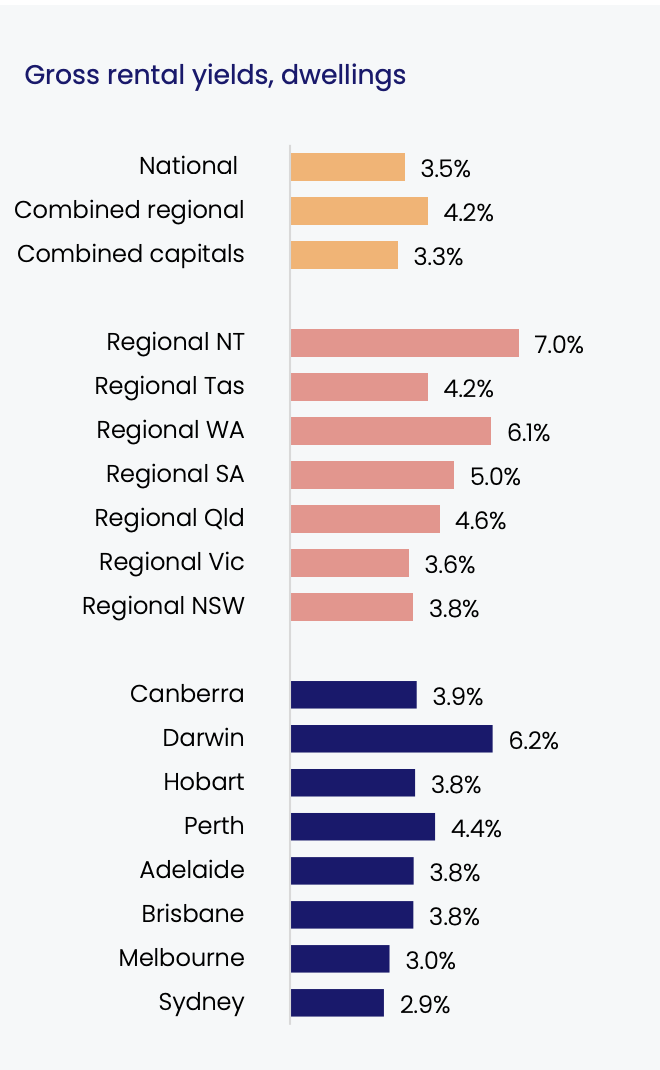

We have seen rents consistently rise while property values broadly trend lower, and gross rental yields are firmly in recovery mode. After capital city gross dwelling yields bottomed out at the record low of 2.96% in February this year, yields consistently rose to 3.29% in August. While capital city yields are still well below the pre-COVID decade average (4.0%), considering the outlook for lower housing values and higher rents, we could see rental yields returning to around average levels over the next year.

Is it time to be greedy when others are cautious? Opportunities are everywhere; many people sell and buy for different reasons. What is essential is that you take your time to choose wisely without the pressure of it being a seller’s market which is precisely the current conditions that a buyer’s market offers.

The Expatriate always tries to make sure all information is accurate. However, when reading our website, please always consider our Disclaimer policy.